The Transforming Healthy Beverage Landscape

As sales of traditional Carbonated Soft Drinks (CSDs) continue to fall and Americans look for healthier alternatives, large beverage companies have responded by both acquiring emerging brands and innovating from within.

Interestingly, however, consumers (and even beverage entrepreneurs) often do not know which brands are owned by the large Beverage Companies, nor do the entrepreneurs appreciate the sheer number of potential buyers for their own companies.

As an investment banker in this space for many years, it is always interesting to take a company to market; so often, we find that a buyer who had been viewed by the seller as a “non-starter” can be the ultimate buyer.

Coke and Pepsi have made several acquisitions in the healthier, emerging beverage brand space: Honest Tea, Zico, Izze, Naked, Odwalla and ONE, for example – and my money is solidly in the camp that the acquisitions have still really just begun. Through these acquisitions, the large strategics bring healthier alternatives to the mass of consumers through more retail channel exposure. Additionally, acquisitions help fuel investment in additional emerging brands. It creates a virtuous cycle. This is all good.

This month, BevNET asked me to lay out this transforming landscape and discuss which beverage companies own which “healthier” (a subjective term, I agree) brands. It turned out to be an interesting exercise. In this article, I also discuss some of the larger, independent beverage companies as well as sizeable, Private Equity-backed ones – perhaps the next wave of brands to be acquired. The exercise unveiled trends, helped solidify thoughts around why certain brands get acquired – and why others do not – and perhaps most importantly, can serve to remind us that the buyer universe for beverage entrepreneurs is far greater than just Coke, Pepsi and Nestle Waters.

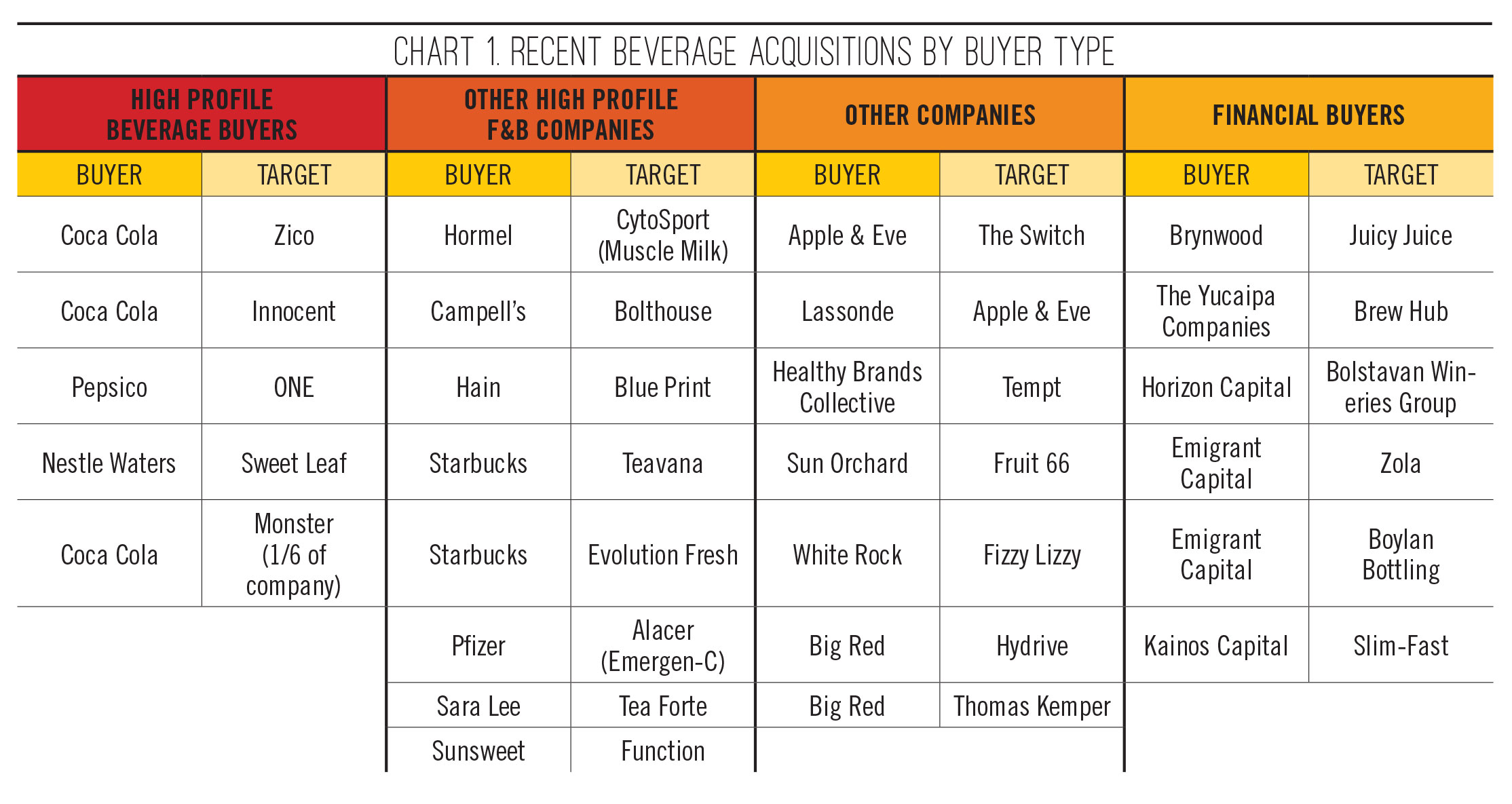

First, let’s take stock of the buyers: To simplify things, I divided them into four buckets: (1) The big three “high profile beverage buyers”– Coca Cola, Pepsi and Nestle Waters; (2) other high profile beverage (and food and beverage) companies: Dr Pepper Snapple, Campbell’s, Hain, Starbucks, Pfizer, Hormel, ITO EN, Sara Lee, Sunsweet, Danone, TATA and Hershey; (3) other companies – a very long list that we put as over 100 companies capable of buying – like Apple & Eve (before they were acquired by Lassonde in June) who acquired The Switch Beverage Co. earlier in 2014; and (4) financial buyers – an important group, as there is over $320 billion of private equity out there looking for a home – or a place to plant a transactional trophy.

Chart 1 below highlights some recent deals by buyer type.

What jumps out there? Nine juice deals: Innocent, Bolthouse, Blue Print, Evolution, The Switch, Apple & Eve, Route 66, Juicy Juice and Zola. Four tea deals: Honest Tea, Sweet Leaf, Teavana and Tea Forte. Three coconut water deals: Zico, ONE and Zola. Within this group, the most notable transactions are Bolthouse ($1.55 billion), Teavana ($620 million) and Cytosport ($450 million); they cover companies in juice, tea, and protein – all hot areas. Compared to those bigger deals, Evolution ($30 million) and Blue Print ($25MM plus earn-outs) seem like the bargains – or premature sells.

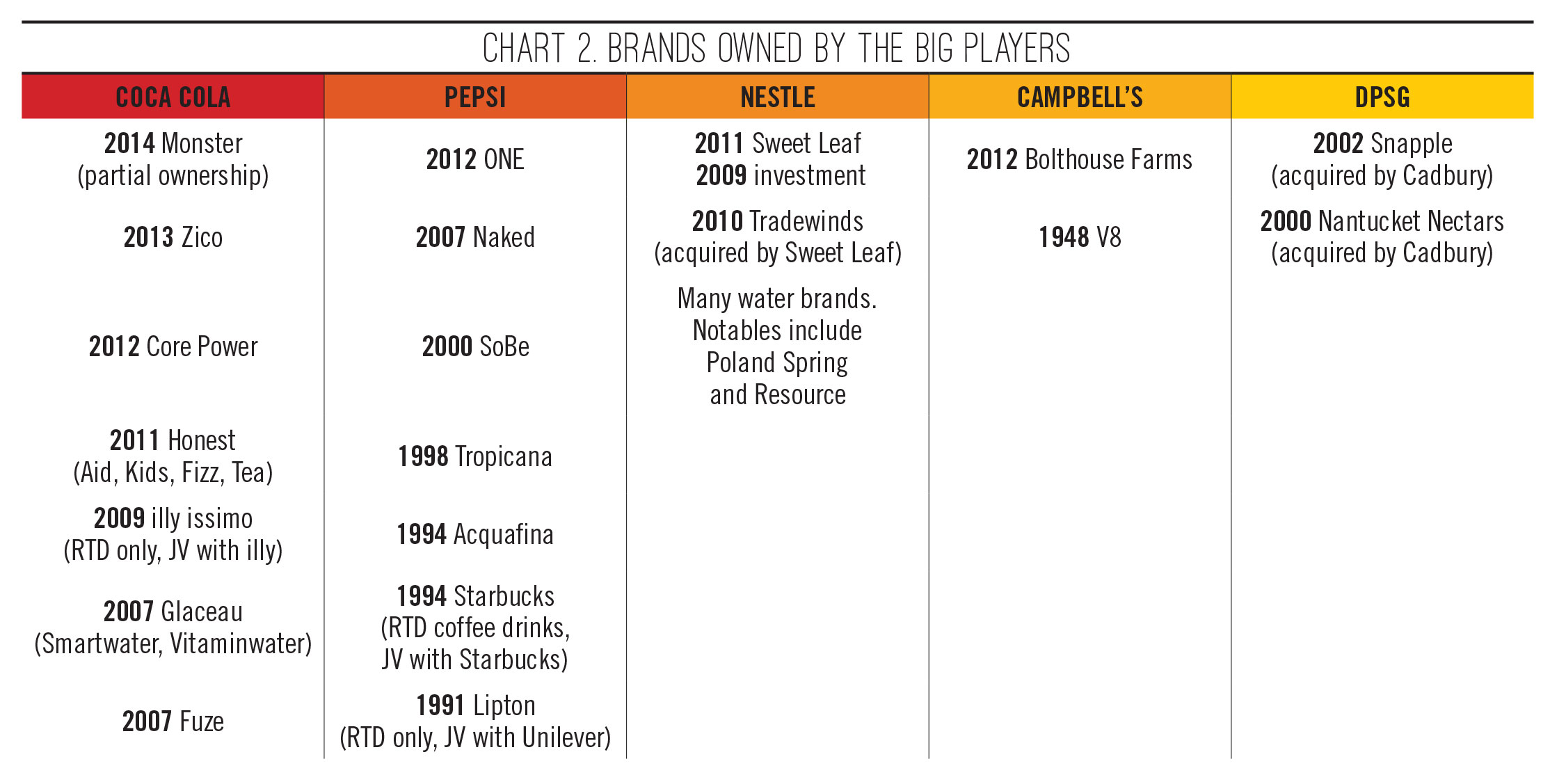

So Who Owns What?

Large beverage companies have been very busy over the last 10 to 15 years with both acquiring and developing their heathier/alternative beverage brand portfolios. Charts 2 and 3 below depict which large beverage companies own which brands (the year indicates what year the brand was acquired – or started internally).

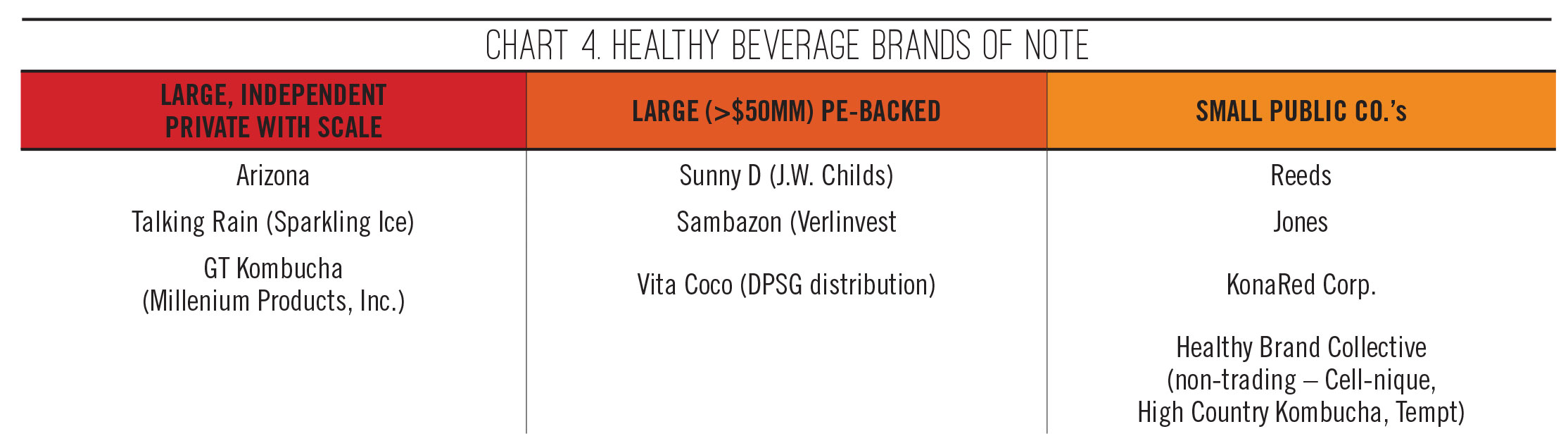

Which Large Brands are Still Out There Solo?

Not every large beverage brand is owned by one of the large, public players though. Although many young companies love to quote the Vitaminwater multiple (as a reality-based investment advisor, I ask you to please stop doing that) or imagine they will be the next Seth Goldman, there are other options out there besides selling. In fact, there are several large independent beverage companies of scale in U.S., and quite a few have more than $50 million in sales, as well as PE-backed companies and smaller public beverage companies as well. Chart 4 below lists just a few examples of the healthier beverage brands of note.

Interestingly, just a few months ago the “Large (>$50MM) PE-Backed” list would have also included Apple & Eve and Muscle Milk. But PE-Backed also means “must sell.”

Over the past four years, at Silverwood Partners we’ve been involved with more than 10 beverage transactions – both sales and investments – with many of those falling under the “not publicly known” category. To be successful, emerging BevCo winners need differentiate and show a path to becoming very large. The beverage data out there is helpful: yes, people need to drink; they want healthier alternatives; they are abandoning traditional CSDs; extending legacy brands further and further no longer works; and almost always, the best innovation comes from outside. Build it, grow it and they will come…

Michael Burgmaier is a Managing Director with Silverwood Partners, an investment bank specializing on the healthy/active living and premium consumer space. 2013/14 announced beverage transactions for Silverwood include The Switch Beverage Co., KeVita, Essentia Water and Spindrift.

Receive your free magazine!

Join thousands of other food and beverage professionals who utilize BevNET Magazine to stay up-to-date on current trends and news within the food and beverage world.

Receive your free copy of the magazine 6x per year in digital or print and utilize insights on consumer behavior, brand growth, category volume, and trend forecasting.

Subscribe