Craft Beer Overview: Breweries Continue to Seek Strength in Numbers

Craft beer has historically held itself as different from many other CPG segments. Primarily, it’s the initial spark that created the business: even as the landscape has become increasingly competitive, craft brewers’ overall position as a better alternative to big beer has long served to give its founders a common bond.

As craft continues to tackle sales declines and lost shelf space, that bond has evolved: now, they’re running in packs.

In the first three months of 2026, we’ve seen a growing set of brands either forming or expanding existing craft brewery platforms or collectives. Craft companies are joining forces to share production capacity, sales teams, back-end efficiencies and more. Whether it’s for survival or for momentum, the strategy is strength in numbers.

Long-time industry watchers have seen it before, like 2008, when Craft Brew Alliance formed, aligning Widmer Brothers and Redhook, and later Kona. Or the mid-2010s, when Artisanal Brewing Ventures (Victory and Southern Tier, and later Sixpoint and Bold Rock Cider) and the CANArchy Craft Brewery Collective (Oskar Blues and Cigar City, and later others) took shape.

The most recent wave of collectivism has been in full swing for a few years now, mainly with regionally based organizations such as Barrel One Collective (Harpoon, Smuttynose, Long Trail and more) in New England, Wilding Brands (Denver Beer Co., Stem Ciders, Great Divide, Upslope and more) in Colorado and Hendler Family Brewing [HFB] (Jack’s Abby, Night Shift and Wormtown)

in Massachusetts.

One of the most recent platforms to join the trend is the Oregon Beverage Collective (OBC), formed in February through the tie-up of several Bend-based bev-alc companies: Crux Fermentation Project, Cascade Lakes Brewing, Silver Moon Brewing, Goodlife Brewing and Tumalo Cider.

Like many of these deals, the structure of the collective isn’t entirely straightforward. The Rhine family, owners of Cascade Lakes, acquired Crux Fermentation from its founders, Larry Sidor and Paul Evers. The two companies remain separate entities, however. Meanwhile, GoodLife, Silver Moon and Tumalo remain privately owned.

Nearly all production for the five companies is transitioning to Crux Fermentation’s production facility in Bend. According to estimates from the Brewers Association (BA), OBC’s collective volume would total more than 40,000 barrels, placing it among the top 60 BA-defined craft breweries in the country.

OBC president Andy Rhine joined the Brewbound Podcast following the deal, and emphasized that OBC’s formation wasn’t out of necessity, even in a Pacific Northwest market facing challenges brought on by distributor consolidation. Instead, the collective’s foundation was built via long-time relationships among the city’s brewery owners and with recognition of rising costs for craft breweries.

Even with a portfolio of five brands and efforts to consolidate production, sales and marketing, Rhine said maintaining each brand’s “unique identity” will be key to the future of the collective, both as a way to foster each brand’s connections with consumers. From a regulatory side, there are also “some advantages with licensing and self-distributing to your own on-premise locations.”

“We see ourselves as roughly doubling the volume of Crux’s facility and there’s also a lot of exciting opportunities with relationships and territory coverage,” Rhine said. “They all have a unique brand identity and they all have some pretty good things going for them, so we’re just trying to accelerate.”

Creating a Loud Voice in Distribution

While addressing capacity space and production costs is core to OBC’s formation, the added volume is also a benefit when dealing with distribution partners.

“Distributors are taking this as a sign of strength, a sign that we’re a stable business and that each brand underneath this portfolio now has more sales and marketing support than they had prior, especially the smaller ones,” Rhine said.

HFB co-founder and CEO Sam Hendler shared similar sentiments during the Brewbound Live business conference in December.

“It’s a totally different conversation when you’re walking into the room to talk about 40,000 cases versus walking into the room talking about 400,000 cases, and you get meaningfully more attention,” Hendler said during a panel discussion with Wilding Brands chief development officer Charlie Berger.

“Chain as well,” he added. “When you have real business working in that chain, it’s way easier to have that dialogue, be aware of opportunities that are coming down the pipeline and be positioned to win.”

HFB was formed out of the contract brewing business Jack’s Abby built to optimize production capacity. Eventually contract brewing clients, such as Night Shift, evolved into acquisition targets.

“As you get into these conversations of people trying to solve real business challenges – and contract brewing was one lever – quickly, certain conversations went to a place where an acquisition just made more sense,” Hendler said.

Having a strengthened relationship with distributors has become even more vital for craft breweries in an era of wholesaler consolidation. In fact, bev-alc distributors merging or swapping brand rights have been hitting the newswire just as frequently as craft deals in the last year, especially in California, one of craft’s largest markets.

The consolidation means some brands – particularly craft beer – have lost some of the attention they were receiving from their boutique distributors pre-consolidation. Having a larger portfolio made up of several brands, sometimes even across several bev-alc categories, can strengthen a collective’s

sticking power.

Still, alignment is complicated. Take Blake’s Beverage, which merged three hard cider brands – Blake’s Hard Cider, Austin Eastciders and Avid Cider Co. – in late 2023.

Like many craft beer collectives, Blake’s operates each of its three brands as three entities with unique identities and intentional portfolios, but with consolidated resources such as production and sales teams. Earlier this year, Blake’s formed a new distribution partnership with Ben. E. Keith Company, which consolidated the company’s Texas network from 19 distributors to one.

“When you have a complex business with a lot of brands and SKUs, creating that internal alignment is super important, so we feel really good about that opportunity,” CEO Andrew Blake said.

But that was just one state.

“It’s gonna be another five years, probably, before we’re truly, fully aligned,” Blake said. “It’s slow and costly, so this takes time.”

Why this Era is Different

There’s a core difference between this wave of groupthink and what has come before: ambition.

Ten years ago, the sky was the limit for craft breweries. Major beer producers were showing that they’d be willing to pay up for brands, and help scale them to national distribution.

In 2015, Constellation scooped up Ballast Point Brewing in an eye-watering $1 billion deal. That same year – also the same year CANarchy was formed, as Oskar Blues Holdings – Heineken grabbed 50% of Lagunitas Brewing. Molson Coors took a majority interest in Saint Archer Brewing, the first of several purchases the macrobrewer would make in the

last decade.

Dozens of other craft deals happened that year, including several purchases by Anheuser-Busch InBev (A-B). Craft was hot, and everyone wanted a piece of the segment’s perceived potential. Platforms provided an opportunity to give even more value to a potential buyer, or the resources to expand just as far without “selling out.” Artisanal Brewing Ventures (ABV) was formed more than a decade ago, and now consists of four core brands: Victory, Southern Tier, Sixpoint and Bold Rock. Around the same time, Oskar Blues Holdings formed with Oskar Blues and Cigar City, later adding Perrin, Deep Ellum, Three Weavers, Squatters and Wasatch.

Ten years later, it’s different. Many of those major brewers have offloaded their craft brands, mainly to Tilray Brands, the global cannabis firm. Tilray acquired four of Molson Coors’ craft offerings and eight craft brands from A-B, likely for pennies on the dollar of their initial purchase prices.

CANarchy was sold to Monster Beverage Corp. in 2022 in a $330 million cash deal. Monster has since written off around $232.4 million of that through several impairment charges, including $51.2 million in Q4 2025.

It’s clear that major craft buyups aren’t happening anymore – again, unless it’s by Tilray, which recently added BrewDog to its lineup in a nearly $54.5 million deal (note: that Scottish brewery was once valued at nearly $2.7 billion). The industry has hit a ceiling: 10,000 craft breweries cannot all garner consumer attention and continue to grow, particularly in a consumer environment that includes more choice than ever across bev-alc bases, styles and price points.

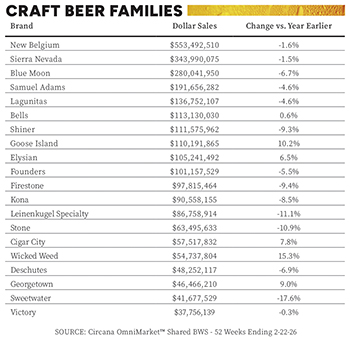

In 2025, both craft beer dollar sales (-4.3%) and volume, measured in case sales (-5.8%) declined yet again, outpacing losses in total beer (dollar sales -2.9%, volume -4.5%) in Circana-tracked multi-outlet plus convenience channels (year-to-date data through December 28).

Through the first two months of 2026, beer dollar sales are about flat (+0.3%), while volume remains in the red (-1.6%). But analysts warn that easy comps from the prior year could be skewing early trends.

In response to several years of declines, craft breweries have turned inward, consolidating distribution footprints, portfolios, teams, locations and more. If big beer or easy sales can’t lift the segment anymore, craft breweries will have to do it themselves.

But it won’t be easy; even with several brands rowing the same way, it can be tough to tell whether it’s on an outrigger canoe, or a life raft.

“If you’re looking to put something like that together, it’ll take twice as long as you think, it’ll be twice as expensive, and the synergies will be probably about half of what you expected at the onset,” Blake said. “People underestimate the complexity of bringing [together] multiple brands, and there’s a real shift of mindset when you go from a branded house to a house of brands.”

Receive your free magazine!

Join thousands of other food and beverage professionals who utilize BevNET Magazine to stay up-to-date on current trends and news within the food and beverage world.

Receive your free copy of the magazine 6x per year in digital or print and utilize insights on consumer behavior, brand growth, category volume, and trend forecasting.

Subscribe