Waves Below the Surface: The Original ‘Healthy Beverage’ Category Gets Roiled by Health and Wellness Concerns

When it comes to health and wellness, consumers’ awareness and concerns about everything from what they eat to what they wear have skyrocketed. Food and drink are increasingly pointed to as both the cause of and the cure for many conditions.

That scrutiny has had ramifications across the beverage space – and even bottled water, the category whose growth as a phenomenon signaled the initial shift of consumers into “healthy beverage” – isn’t immune.

As consumers grow more concerned about environmental toxins like microplastics, adopt GLP-1 drugs that transform their diets and educate themselves on the importance of routine hydration, the way they’re approaching the bottled water category is transforming, from the packaging formats they’re most likely to buy to the amount they purchase.

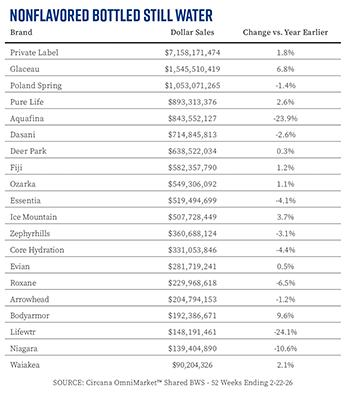

Amidst these crosswinds, the category is relatively stable. Market research firm Circana reported that sales of the $17.6 billion unflavored, bottled still water category in U.S. MULO and c-store accounts were down by 0.6% in the 52-week period ending December 28, 2025. However, in a sign that stocking up is beating out single-serve purchasing, bulk still water products were up 3.2% in the same period to $2.7 billion.

But that surface stability hides shifts, according to Nick McCoy, co-founder and managing director of Whipstitch Capital. Channel matters, he said, and individual brand performance is varying widely.

Water is also increasingly playing a role in the diets of health-conscious consumers, McCoy observed. The recent focus on hydration and GLP-1 use are tailwinds for this often all-too-plain category. Combined with an uncertain economy, consumers are changing how and where they pick up their bottled refreshment.

“I’ve seen shifting GLP-1 data where, within the last year or a few months, it was showing [users make] more trips to convenience stores,” McCoy said. “And the latest data I saw [in March] was more trips to mass and less trips to convenience.”

With health and budget both at the top of mind, there’s plenty to unpack in bottled water.

Pack in Action

From fueling growth for emerging brands like PATH to top-down affirmation from the Primo Brands portfolio, water companies of all sizes are continuing to lean on aluminum as a way to attract both eco- and, increasingly, health-conscious consumers.

Nicole Doucet, CEO of aluminum bottle and canned water brand Open Water, said that while sustainability remains the company’s “North Star,” oftentimes today the brand has found that it’s attracting consumers more concerned about the health impact of contaminants like microplastics than it is shoppers worried about the environment.

For Open Water, which completed a comprehensive rebrand around a year ago, those health concerns are an opportunity to introduce itself to consumers and begin selling them on its bigger mission and positioning as an environmentally friendly business.

“I see the health conversation as a bonus, as a way to get people to maybe dig a little bit deeper and realize that the impact goes beyond just them,” Doucet said. “We’re worried about the bigger issue, or the complete issue, and the health thing is sometimes the beginning of people digging into this.”

Environmental researchers, such as those at Pennsylvania State University, will note that microplastics primarily enter water systems at the source, and can impact both tap and bottled water. Nevertheless, many consumers will still veer away from PET bottles due to associations or concerns around plastic leeching into their beverages. A 2025 study from Concordia University appeared to vindicate those concerns, finding that the average person will consume between 39,000 to 52,000 microplastic particles annually, but people who drink bottled water will take in around 90,000 more particles each year.

Reza Mirza, global CEO of Icelandic Glacial, said he’s seen similar concerns around microplastics and PFAS chemicals driving consumer behavior, noting that the brand’s glass business is “on fire” as people seek out better-for-you packaging solutions.

However, Mirza cautioned that plastic is still the dominant force in the category – and for the company: glass only makes up around 15-20% of Icelandic Glacial’s business.

“Right now, PET is still the biggest driver for bottled water,” he said. “Once you just step back from all the noise, all the nonsense – What really drives consumption of bottled water? It is convenience. And there is still no other material out there which offers the convenience of plastic.”

Beyond traditional retail, the health and environmental concerns are also continuing to push on-premise accounts to embrace alternative packaging. As Doucet suggested, there’s no shortage of businesses across industries that are ripe targets for new accounts, noting that Open Water has recently added both theme restaurant chain Medieval Times and “hot tub yacht” tour companies to its customer list as hospitality and entertainment businesses seek to provide better, premium offerings to their consumers.

For a smaller emerging brand like Open Water, brand building on-premise can also pose a challenge. One aluminum competitor, PATH, has carved out a unique revenue stream for itself by creating customized, co-branded bottles for its murderers’ row of high end hospitality partners, Open Water plans to lean on its core packaging wherever it goes to build brand equity and to maintain its core messaging.

“I think that when you’re making the switch away from plastic, oftentimes you’re switching from something that is very cheap to something that’s slightly more expensive,” Doucet said. “So you want a brand that’s gonna tell that story, right? Just tell the ‘why’ behind it. I think that we’ve done a very good job there.”

While cans as a format for still water has declined in recent months, Doucet, suggested that her brand and others are continuing to see growth for aluminum cans, but the decline of Liquid Death’s flagship still water has had an outsized drag on the segment. According to NielsenIQ, retail dollar sales of Liquid Death’s still water line was down 17.8% in the 52-week period ending March 7, 2026, with volume dropping by 21%, as the brand has apparently focused more effort on its fast growing sparkling water and iced tea lines.

More Occasions, More Opportunities

The health mindset is also opening up new occasions for water brands.

Shadi Bakour, CEO of PATH, suggested that as “we’re seeing alcohol plummet, it just creates more of an opportunity for your average person to be consuming more water.”

While Bakour said he doesn’t see alcohol as a competitor for PATH – single-use plastic brands are still its primary competition – the health occasion has opened the door for new marketing opportunities for brands to execute on.

“Consuming more water, creating more hydration, leads to just everything in life that’s good – more productivity, weight loss, it’s really simple to think that you can just drink more water and that’s the solution. But it’s such an impactful thing.”

PATH, which was founded in 2017, has been rapidly adding to its list of marketing activations, partnering with pro sports teams, gym chains, airlines and cruise liners, Bakour said.

“We’ve built the base now for us to really lean in, continue to expand and develop and what we’ve done over the past [several] months is we’ve focused a lot on honing in on our team and we’ve brought a ton of talent to the organization, so that is allowing us to evolve and really operate as a highly effective and winning organization,” he said.

At Icelandic Glacial, which Mirza says operates on a shoestring marketing budget in order to focus its funds on execution, bottled water brands still have large opportunities ahead to balance broad health and wellness messaging with premium lifestyle campaigns. For Icelandic, that means global activations with designers at Paris Fashion Week and events like the South Beach Food and Wine Festival.

“If I’m a brand, I would want to be in the premium water space, but I’ve got to have a story,” he said. “I’ve got to have significant strength behind it. Just premium pricing on purified water in a nice package is not the whole thing for a brand to be successful. The whole thing has to come together.”

Receive your free magazine!

Join thousands of other food and beverage professionals who utilize BevNET Magazine to stay up-to-date on current trends and news within the food and beverage world.

Receive your free copy of the magazine 6x per year in digital or print and utilize insights on consumer behavior, brand growth, category volume, and trend forecasting.

Subscribe