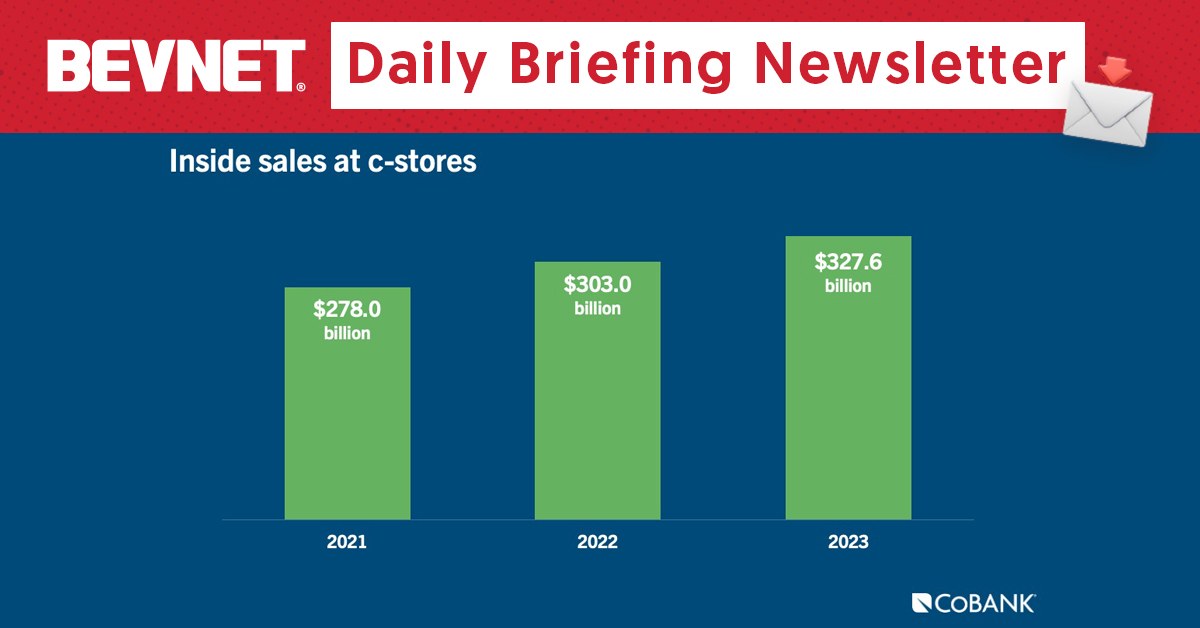

In 2020, for reasons that should probably be obvious to everybody by now, foot traffic in the convenience channel plummeted. But times have quite thankfully changed and traffic is back up (+58.6% since January 2021, to be precise) as in-store sales surpassed $327.6 billion annually.

While traffic returned to a normal frequency, drivers to get consumers in the door have largely shifted with demand for foodservice items on the way up, according to a CoBank report last week.

On their way down, however, are CPG brands. Circana tracked a dollar sales decline of 2.4% in the c-store channel in Q3 2024, while inversely rising 2.4% in MULO. That drop reflected a lower number of convenience store trips per buyer on a year-over-year basis, but a rise in dollars spent per trip.

The allure of prepared food is making a particularly big impact to get shoppers out of their cars and into the store, with foodservice representing 26.9% of all in-store sales – up 1.3% year-over-year. That includes hot, cold and frozen beverages.

Big brands have certainly been paying attention to these trends, and they’re looking at partnerships and promotions that can help move cans alongside fresh food. For example, energy drink brand Celsius embraced a meal deal promotion with Casey’s stores last fall to combo a can of Celsius with hot pizza.

Celsius CEO John Fieldly told us in an October interview that the company is seeing more retailers seek out food and energy drink pairings, noting that internal data has shown its consumer is more likely to purchase “incremental food items” when buying a can of Celsius.

Other brands are embracing the change by innovating around ready-to-serve products: KDP recently added Snapple Zero Sugar Peach Tea to its dispensed beverage offerings at 7-Eleven stores, marking the first time the brand has been available in this format.

CoBank noted that c-store chains are increasingly competing with quick service restaurants and fast food. For CPG brands playing in the space, there may be a benefit to thinking of convenience not just as a retail opportunity, but as an on-premise play.