Protein Proliferates Even As People Drop Pounds

In the modern functional beverage era, products aligned with niche ingredients and attributes easily fall in and out of fashion. Even vital macronutrients such as carbohydrates and fats have been on the outs at times, but protein remains a nutritional evergreen: While the industry is well within a functional “protein plus” beverage wave, experts claim we may never find the point of “peak protein.”

“Protein continues to be a health halo,” emphasized Scott Dicker, senior director of market insight at SPINS. “As we see more and more consumers interested in health… they’re consuming more and more information around [protein] and it is changing a lot of their daily routine.”

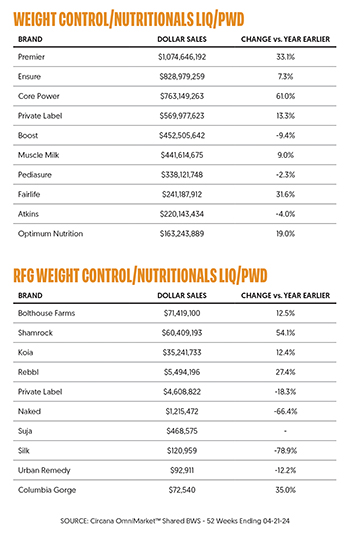

That interest is reflected in increased sales and M&A activity: Total dollar sales for the liquid protein and meal replacement category totaled $5.3 billion, a 13.9% increase, according to recent Circana data for the 52-week period ending April 21, 2024. The growth was supported by significant volume/unit share gains of 11.2%.

Within that landscape, everyone from legacy, leading players like Bellring Brand’s Premier Protein to disruptive concepts like plant-focused Only What You Need (OWYN), which recently sold to Simply Good Foods, have seen upward volume momentum. Premier remains at the top, locking in over $1 billion in sales (+33%) for its shelf-stable milk protein and meal replacement products while volumes grew 24% and average prices increased 7.3% in the past year, according to Circana.

At the heart of the expansion is increased consumer awareness around the value of protein. While shakes have long served as the entry point for innovations designed around new dietary habits and health hacks, protein’s position for every person’s diet has expanded, giving it permission to tap newly interested, growing, slimming and aging populations.

“If I were to put my finger on one point of why it’s growing so fast, it is because we’re seeing an influx of new demographics – these are for women and then also for the aging population,” said Dicker. “It’s not just for young people. We’re seeing the increased importance of higher protein for aging populations to preserve muscle mass, which will keep them healthier, longer.”

Barb Stuckey, chief innovation and marketing officer at Mattson, also echoed this point by noting that protein beverages are growing alongside increasing consumer interest in longevity and lifespan, in addition to a rising use of GLP-1 drugs like Ozempic. As more consumers embrace health-forward mindsets in a post-pandemic world, protein’s appeal, and the category’s marketing efforts, are expanding the space further beyond muscle building and satiety claims to new groups and use occasions that have the ability to grow the entire segment.

“The marketing has moved away from having a bodybuilder bench pressing, to people going about their daily life – that’s really had an impact,” said Dicker. “We also see a lot of tailwinds for a lot of reasons: now there’s an increased demographic coming in, they’re interested in it for different reasons, they’re familiar with it, and you see it proliferating across the entire grocery store.”

Planting New Seeds

One novel aspect of the protein boom is that the source base of the protein has broadened to include more vegan materials. Overall, plant-based protein sales have held their own against animal-based counterparts, increasing 36.5%, compared to the animal-based subcategory’s 31% growth over the past year. Plant-based shake maker OWYN has generated over $69 million in total sales in SPINS tracked channels alone, a 119% jump as volumes grew 82% and average prices rose 20%.

Joshua Schall, a consultant who works with brands in the nutrition space, believes that many plant-based products have advanced to a point where consumers feel they are near parity in terms of flavor and texture to animal-based beverages. OWYN’s acquisition in April signals strong future growth potential for the segment, with prospects that have been enhanced by distribution and marketing efforts as well as a broadening consumer base.

“There’s an overarching secular trend towards people making more conscious decisions around animal products over plant products, and that’s not necessarily attached to this category, but just across CPG,” Schall said. “If you look at it over [a short term period], the overall consumption change is probably not that big, but if you look at it from an incremental 1% over long periods of time you make huge differences across a bunch of different categories.”

As OWYN built up its core consumer, it did not try to go after the typical plant-based shopper and worked to broaden its appeal beyond the natural channel, with the product and branding in line with conventional protein products. This position enabled OWYN to convert new consumers to both plant-based products and the protein category, Schall said.

“There’s a lot of trends moving in the positive direction for plant based proteins,” Schall added. “Is it something that’s going to grow huge leaps and bounds year over year? Maybe not, but I think it’s one of those [segments] that does provide a consistent, probably above average compounded annual growth rate. It’s a good space to build in if you’re patient.”

Plant-based Proteins Bring Brands Across Category Lines

According to Henry Kasindorf, as the segment has evolved, Remedy Organics, which was founded in 2017, has positioned itself around a variety of attributes from keto to gut health. But the brand’s latest innovation goes deep on protein. The newly launched Power Shakes variety ups Remedy’s original protein content to 20 grams per bottle via three indulgence-aligned flavors: Cold Brew Latte, Vanilla Dream and Chocolate Fudge; the coffee flavor also contains 80 mg of caffeine.

“Not only are we leaning into these really clean, high protein beverages, but we’re doubling down,” said Kasindorf. “This line is really based on the data and insights that we have, it is what consumers really want and we’re excited about it. The retailer’s response to it has been very strong as well and [with this launch] we will have the shake with the highest levels of protein in the refrigerated category.”

The brand is positioned toward a natural shopper, but has nevertheless seen significant growth in the mass channel and is currently sold in 20,000 doors nationwide. Remedy has seen volume growth of 38% and dollar sales increase 36% in MULO compared to a year ago, according to Kasindorf. He said the brand’s flavor and functional innovation, as well as its added prebiotic and energizing benefits have allowed it to garner widespread appeal.

“When we launched we were doing well in natural channel retailers, but we didn’t know if it was going to work in more conventional channels,” said Kasindorf. “We continued to push the envelope relatively early in mass, in drug and c-stores and… it has worked everywhere.”

Even legacy players are turning to plants. Muscle Milk debuted its Muscle Milk Plant line earlier this year in three indulgent varieties made with 30 grams of pea, rice and canola-derived protein. Even though parent organization Cytosport (owned by PepsiCo) also produces plant-based protein shake Evolve, a spokesperson for Muscle Milk said that the new launch is a way to keep consumers shopping within the Muscle Milk “family.”

Innovation in the category is also being accelerated now that production line time has opened up after being largely constrained during the pandemic. Co-manufacturing capacity limitations hindered innovation activities during the pandemic, Schall said, but now that those bottlenecks have been cleared both large companies and startups have more opportunity and incentive to experiment.

“There’s already been a number of different announcements that have started to leak that [other brands] are working on RTD protein shakes or in development…these are brands that have been incubated and sitting there waiting to deploy some brand equity in a beverage format,” Schall hinted. “Within the next six to 12 months that will likely start to play out so 2025 looks pretty interesting.”

GLP-1 Drugs’ Impact On The Innovation Cycle

One other factor is expected to buoy protein drinks’ fortunes: the growth of GLP-1 drugs like Ozempic. Among GLP-1 drug users, the demand for convenient protein-packed products is anticipated to be strong, but there are other effects that will likely reverberate across the category.

“We’re talking about convenient nutrition and convenience is a big part of this whole thing,” said Schall. “Just knowing that you need more protein is great, but then actually having the options to do it in a way that is not going to bend your typical lifestyle – that’s where these products play up even more because they can serve a purpose across the board for people that seek or need convenience.”

Dicker and Schall noted that consumers will increasingly reach for products that fill nutrient gaps – like superfood powders, green powders and multivitamins. He explained that protein products that have added fiber will also be important to this consumer demographic due to the impact these drugs have been reported to have on digestive function.

While these diet-drugs have created a new protein shake consumer demographic, legacy products are also being retrofitted to meet emerging needs. Atkins, which was designed around a low carb diet for weight loss, is now, nearly 35 years later, being revitalized for consumers using GLP-1 drugs like Ozempic and seeking a protein boost to combat excessive muscle and weight loss. This expanding consumer group will also likely drive a category expansion, said Stuckey.

“My gut is that this is a new consumer to the category – I don’t think these consumers were protein shake users until they started to go on these drugs and went to the doctor [as] they’re rapidly losing weight rapidly and their doctor said, ‘You need to eat more protein,” said Stuckey. “One of the doctors we talked to said, ‘I cannot believe I’m actually suggesting that people drink protein shakes. But I am suggesting that to these people [using GLP-1s].”

Protein Shakes Walked So Protein Water Could Wander In

Overall, the interest in protein – whether it is for muscle building, longevity, a complement to weight loss or other interests – has pushed protein contents in products to new heights. High and ultra-high protein products are finding their way to market with some containing upwards of 30 grams per serving; brands like OWYN, Premier, Huel, Fairlife and Muscle Milk all have high protein products. Schall believes there may now be more opportunity to capture consumers at the lower end of the spectrum, and with more refreshing, less dessert-heavy flavors.

The desire for less sugar-intensive products has led to a new wave of protein beverages, sometimes referred to as protein waters. Vita Coco launched its PWR LIFT brand in 2022, a clear sugar-free liquid infused with whey, that comes in four flavors: Berry Strawberry, Lemon Lime, Blueberry Pomegranate and Orange Mango.

This is not a novel category. Brands such as Protein2o have been around since 2013 and garnered nearly $7 million in total dollar sales in the past year, according to Circana. But Stuckey emphasized that the whey protein previously used in these types of products produced an unpleasant mouthfeel – a challenge that has been mitigated as industry stakeholders made significant investments in recent years.

Protein waters may also be important to the aforementioned GLP-1 crowd, who are seeking increased protein and hydration products, according to a recent study among 70 GLP-1 users conducted by Mattson. Though these products may meet the emerging needs of the niche consumer demographic, Stuckey and Schall believe they have widespread appeal and expect to see the protein water format expand across consumer demographics.

Stuckey noted that while the whey protein material used in these formulations have been improved, there isn’t currently a comparable plant-based protein option available that is palatable in clear liquids, leaving room for future disruption in the emerging category.

“The plant based proteins that have been acidified in this way to allow for refreshing clear averages are almost inedible,” Stuckey said. “They are not ready for primetime yet…so there’s a lot of opportunity for suppliers here. And this is segues into the Ozempic opportunity because what we hear from the patients is that they don’t feel good when they eat these really big creamy shakes. They’re having trouble with feeling full already…so that’s where these clear protein beverages can really play a role.”

Receive your free magazine!

Join thousands of other food and beverage professionals who utilize BevNET Magazine to stay up-to-date on current trends and news within the food and beverage world.

Receive your free copy of the magazine 6x per year in digital or print and utilize insights on consumer behavior, brand growth, category volume, and trend forecasting.

Subscribe